As geopolitical tensions in West Asia escalate, the ripple effects are being felt deeply across the Indian subcontinent. For an economy that imports over 85% of its crude oil and relies on the Suez Canal for more than a third of its international trade, the stakes are exceptionally high. This report analyzes the direct impact on India's macro-indicators and fixed-income markets.

The Crude Reality: Oil-Driven Inflation

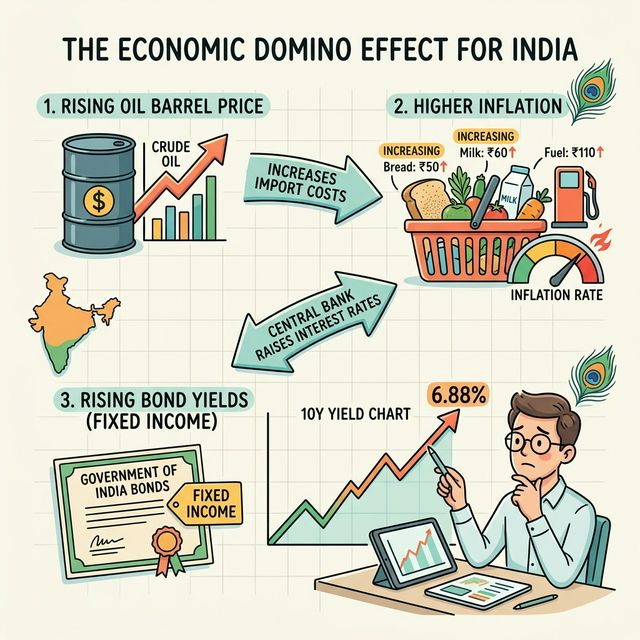

The surge in Brent crude prices (reaching near $87 per barrel in early 2026) poses a significant risk to India's fiscal stability. Every $10 increase in oil prices traditionally widens India's Current Account Deficit (CAD) by approximately 0.3 to 0.4 percent of GDP. This is not just a statistical concern; it translates to over $10 billion in additional import costs annually.

| Metric | Impact of $10 Oil Hike | Current Estimate |

|---|---|---|

| Current Account Deficit | +$10 Billion | Widening to 1.5% of GDP |

| Consumer Price Inflation | +20-25 Basis Points | 5.4% (Forecast) |

| USD/INR Exchange Rate | -1.5% to -2% | ₹93.97 (Historical Low) |

| GDP Growth | -0.3% to -0.5% | 6.5% - 6.8% |

[!IMPORTANT] A sustained period of oil above $95 per barrel could threaten the RBI's glide path toward its 4 percent inflation target. This would potentially delay interest rate cuts into late 2026 as the central bank prioritizes price stability over growth.

Sector-Specific Vulnerabilities

The impact is not uniform across the Indian economy. Several key sectors are facing immediate margin pressure due to the dual blow of energy costs and logistical hurdles.

- Fertilizers and Chemicals: India relys on the Middle East for essential raw materials like rock phosphate and sulfur. Supply disruptions here can lead to higher input costs for Indian farmers, potentially increasing the government's subsidy burden.

- Gems and Jewelry: With the Middle East being a major destination for Indian jewelry exports, any regional slowdown directly affects the demand for high-value merchandise.

- Automotive and Electronics: These sectors are part of global just-in-time supply chains. Delays in receiving components through the Red Sea are forcing manufacturers to maintain higher inventory levels, which ties up working capital.

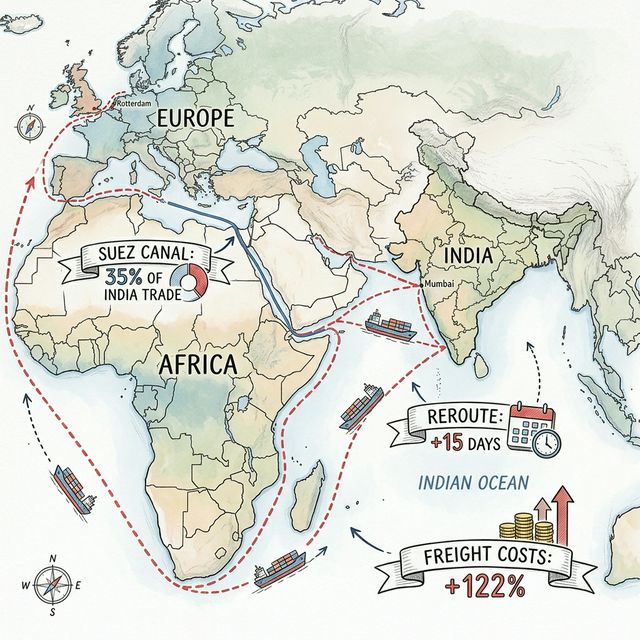

Trade at a Crossroads: The Suez vs. Cape Route

The Red Sea crisis has transformed the Suez Canal from a vital artery into a bottleneck. Rerouting ships around the Cape of Good Hope has surged freight costs by over 120 percent, effectively adding a "geopolitical tax" to Indian exports. This rerouting adds between 10 to 20 days to the transit time, making Indian goods less competitive in European markets.